All good? Or is it?

Commentary by Prof. Dr.-Ing. Thomas Wimmer, Chairman of the Board, BVL - The Supply Chain Network

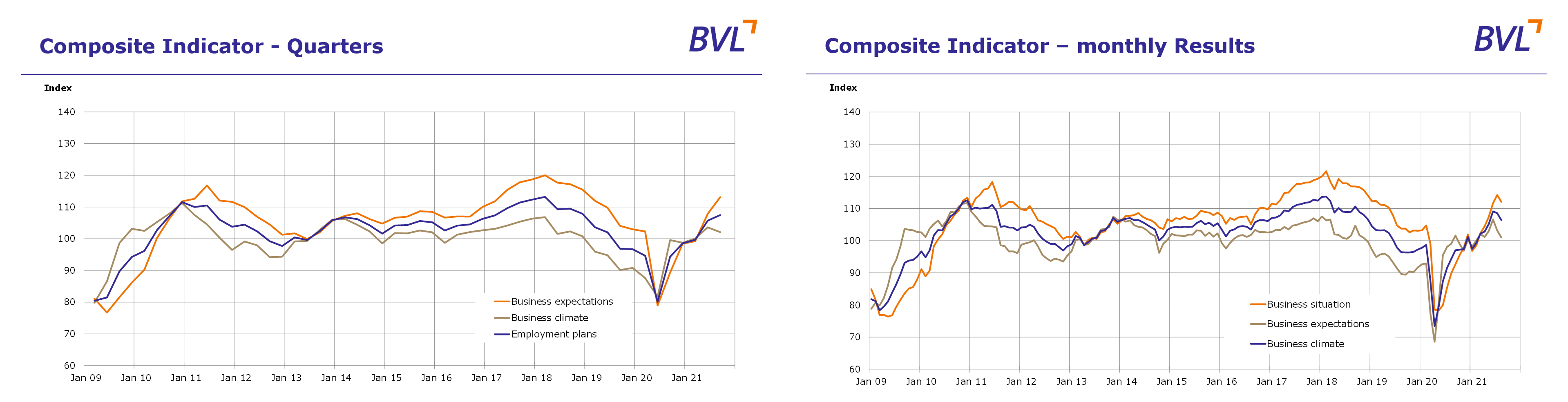

The good news brought to us by the Logistics Indicator for the 3rd quarter of 2021 is this: the pandemic may still not be over, but the scores of the respondents for the current business situation, business expectations and therefore also for the business climate are back to the pre-corona levels of 2018 and 2019 – but only if we aggregate the survey findings for the months June, July and August to form quarterly scores. The picture is not nearly as bright, however, if we consider the August figures in isolation. It is particularly in recent weeks that we have seen a significant deterioration in assessments of the current business situation and above all in expectations for future business – in industry, in trade and among the logistics service providers.

Despite a robust current business situation, the momentum from the month of June is gradually dissipating. The smooth V-shaped course of the indicator curve promising rapid recovery is beginning to look shaky – although the logistics service providers report a favourable demand trend, rising prices and new personnel recruitment. Industry and trade are also signalling that they are looking for new personnel. At the same time, however they are reporting low stock levels and rising prices.

At the end of August, the German Bundestag parliament confirmed the legislation on what is calls the “epidemic situation of national significance”, and the corresponding laws will remain in place into the autumn. Ultimately, however, it is the concrete economic challenges that raise doubts over the recovery of the economy. In July, for example, the German Association of the Automotive Industry (VDA) downgraded its sales forecast for 2021 from eight to three percent. The reason? A lack of electronic components. But it’s not only “chips” that are in short supply and causing production downtime. All industries are facing scarcities and rising prices for input products like steel, timber and other construction and raw materials as well as energy. As the Federal Statistical Office noted in August, the producer prices for industrial products in July 2021 were 10.4 percent higher than in July 2020. This was the biggest year-on-year rise since January 1975 (+10.5%), when prices showed a marked increase in connection with the first oil crisis. Volume and price fluctuations together with uncertain forecasts have a particularly serious impact on the logistics sector.

The good news is that the phase of short-time work is almost over, and we are now seeing stability in the labour market. GDP in Q2 was just 3.3 percent lower than in the last pre-corona quarter at the end of 2019. Broad areas of social and economic life are returning to their former status or effectively adapting to a “new normal”.

The vaccination campaign is having its effect, and the health risks are lower for those who are immunised and continue to act responsibly – and this means that we can once again return to our accustomed, or slightly modified, processes. This also means that people can come together again; it paves the way for the direct encounters and communication that we have all missed for so long. The audits for the German Award for SCM and the MX Manufacturing Excellence Award, for example, took place on site at the companies whose concepts were nominated.

BVL is doing everything it can to be able to stage the International Supply Chain Conference from October 20 to 22. The plan is for an event that will make use of digital elements to share information while also kick-starting a live, vibrant and in-person.

|

Downloads

- Detailed results ( PDF, 532 Kb)

- Commentary by ifo Institute, Prof. Wollmershäuser ( PDF, 108 Kb)

- Commentary by BVL's President Prof. Thomas Wimmer ( PDF, 24 Kb)